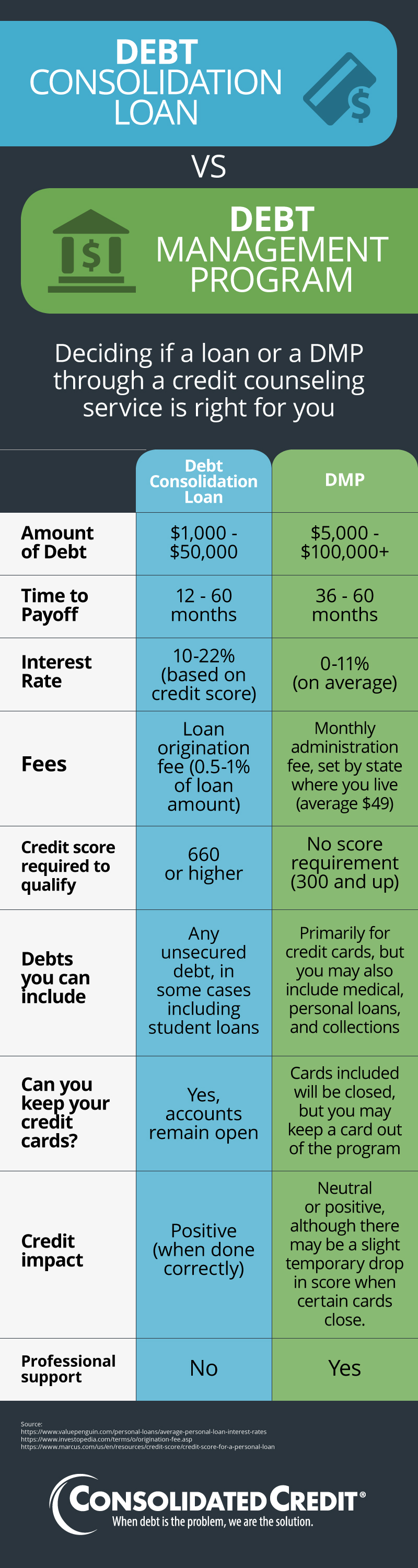

Consolidating debt has many benefits. Consolidating debt can lower interest rates, improve credit scores, and simplify your repayments. It is crucial to understand the pros and cons of debt consolidation. This article will examine the pros and cons of debt consolidation. A debt consolidation loan can reduce interest rates, but it may also raise payments.

Lower-interest debt consolidation reduces interest charges

A lower-interest consolidation loan for credit card debt can help you pay your bills more quickly. It can also help you reduce the number of bills that you have accumulated since the recent economic crisis. Here are some tips for debt consolidation.

By consolidating your debts into one low interest loan, you can reduce interest rates and lower your monthly payments. This will reduce your credit card debt and prevent collection calls. It is important to remember that you will temporarily lose your credit score by applying for a loan. When you are diligent about your payments and clear your credit cards, debt consolidation can help improve your credit score.

It can help improve your credit score

If you're in debt, you may be wondering whether debt consolidation can improve your credit score. How you approach debt consolidation will determine the answer. There are many options. One is to take out a new credit card or loan. This lowers your score. Negotiating a lower payment is another option. You will need to consider your credit score, credit utilization ratio and payment history before deciding if debt consolidation is right for you.

Your payment history can affect your credit score. That is why it is important that you pay on time. The initial credit score of a debt consolidation loan will be lower, but the new monthly installment will be easier. Because your payment history makes up 35 percent of your credit score, paying on time can improve your credit score.

It can streamline repayment

Debt consolidation is a good option for those who want to manage their payments more easily. People can lower their monthly payments with debt consolidation. They combine all their debts into a single loan/credit card. This allows them to use the funds of this account to pay down their old balances. This allows them to make their repayments more manageable and also improves their credit score.

Online or through a credit union or bank, you can apply for a consolidation loan to consolidate debt. Funds may be available within a few days of approval. You can use this money to pay off your current debts, or the lender can pay them off directly.

It can raise your payments

You may be wondering if debt consolidation might be right for you. You will pay a lower monthly amount and have a lower interest rate with debt consolidation. Comparing multiple loan options will help you find the best one for your needs. A debt consolidation service can help you decide the repayment term that is best for your financial situation. While shorter repayment terms may result in higher monthly payments, they can also save you more over the life of your loan. Consolidation is also beneficial as a debt management tool because it allows you to plan your finances better and reduce your monthly payments.

While debt consolidation might seem like a great solution, there are also some drawbacks. High interest rates are the main problem. Consolidating your debt can help you pay down your debts faster. Consolidating your debt means you have one lender and not several.

It can raise your interest-rate

While a consolidation loan offers a lower monthly repayment, it can also come at a significant cost. Prepayment penalties and origination charges are common for debt consolidation loans. These fees can decrease the savings due to the lower interest rates. These fees usually range from one to five percent on the total loan amount. Before you apply for a consolidation loan, make sure to carefully examine the terms and conditions.

If you fail to pay your credit card bills on time, your interest rate may be raised by the credit card company. While consolidating debt with loans may reduce your credit score, they can make it easier to pay off your credit cards. For this reason, it is important to carefully plan your monthly budget. You can also use autopay and other methods to avoid missing a payment. Communicate with your lender if you have any other circumstances that could lead to you missing a payment.

FAQ

Why is personal financing important?

Anyone who is serious about financial success must be able to manage their finances. We live in a world that is fraught with money and often face difficult decisions regarding how we spend our hard-earned money.

Why then do we keep putting off saving money. What is the best thing to do with our time and energy?

The answer is yes and no. Yes because most people feel guilty about saving money. Yes, but the more you make, the more you can invest.

Focusing on the big picture will help you justify spending your money.

You must learn to control your emotions in order to be financially successful. Negative thoughts will keep you from having positive thoughts.

You may also have unrealistic expectations about how much money you will eventually accumulate. You don't know how to properly manage your finances.

Once you've mastered these skills, you'll be ready to tackle the next step - learning how to budget.

Budgeting is the act or practice of setting aside money each month to pay for future expenses. Planning will allow you to avoid buying unnecessary items and provide sufficient funds to pay your bills.

Now that you understand how to best allocate your resources, it is possible to start looking forward to a better financial future.

Which side hustles are the most lucrative in 2022

To create value for another person is the best way to make today's money. If you do this well the money will follow.

Even though you may not realise it right now, you have been creating value since the beginning. When you were a baby, you sucked your mommy's breast milk and she gave you life. Learning to walk gave you a better life.

If you keep giving value to others, you will continue making more. In fact, the more you give, the more you'll receive.

Everyone uses value creation every day, even though they don't know it. Whether you're cooking dinner for your family, driving your kids to school, taking out the trash, or simply paying the bills, you're constantly creating value.

In reality, Earth has nearly 7 Billion people. This means that every person creates a tremendous amount of value each day. Even if you create only $1 per hour of value, you would be creating $7,000,000 a year.

That means that if you could find ten ways to add $100 to someone's life per week, you'd earn an extra $700,000 a year. This is a lot more than what you earn working full-time.

Now let's pretend you wanted that to be doubled. Let's imagine you could find 20 ways of adding $200 per month to someone's lives. You'd not only earn an additional $14.4 million annually but also be incredibly rich.

Every day offers millions of opportunities to add value. This includes selling information, products and services.

Even though we focus a lot on careers, income streams, and jobs, these are only tools that can help us achieve our goals. Ultimately, the real goal is to help others achieve theirs.

Focus on creating value if you want to be successful. My free guide, How To Create Value and Get Paid For It, will help you get started.

How much debt can you take on?

It is essential to remember that money is not unlimited. You will eventually run out money if you spend more than your income. Because savings take time to grow, it is best to limit your spending. So when you find yourself running low on funds, make sure you cut back on spending.

But how much should you live with? There is no universal number. However, the rule of thumb is that you should live within 10%. You'll never go broke, even after years and years of saving.

This means that you shouldn't spend more money than $10,000 a year if your income is $10,000. If you make $20,000, you should' t spend more than $2,000 per month. For $50,000 you can spend no more than $5,000 each month.

It's important to pay off any debts as soon and as quickly as you can. This includes student loans and credit card bills. Once these are paid off, you'll still have some money left to save.

It is best to consider whether or not you wish to invest any excess income. If you choose to invest your money in bonds or stocks, you may lose it if the stock exchange falls. However, if the money is put into savings accounts, it will compound over time.

For example, let's say you set aside $100 weekly for savings. In five years, this would add up to $500. After six years, you would have $1,000 saved. In eight years, you'd have nearly $3,000 in the bank. In ten years you would have $13,000 in savings.

You'll have almost $40,000 sitting in your savings account at the end of fifteen years. It's impressive. But if you had put the same amount into the stock market over the same time period, you would have earned interest. You'd have more than $57,000 instead of $40,000

This is why it is so important to understand how to properly manage your finances. If you don't do this, you may end up spending far more than you originally planned.

How to make passive income?

To make consistent earnings from one source you must first understand why people purchase what they do.

It is important to understand people's needs and wants. Learn how to connect with people to make them feel valued and be able to sell to them.

You must then figure out how you can convert leads into customers. You must also master customer service to retain satisfied clients.

Every product or service has a buyer, even though you may not be aware of it. And if you know who that buyer is, you can design your entire business around serving him/her.

It takes a lot of work to become a millionaire. You will need to put in even more effort to become a millionaire. Why? Why?

You can then become a millionaire. Finally, you must become a billionaire. The same goes for becoming a billionaire.

How does one become a billionaire, you ask? Well, it starts with being a thousandaire. You only need to begin making money in order to reach this goal.

But before you can begin earning money, you have to get started. Let's look at how to get going.

What's the difference between passive income vs active income?

Passive income can be defined as a way to make passive income without any work. Active income requires effort and hard work.

Active income is when you create value for someone else. Earn money by providing a service or product to someone. Examples include creating a website, selling products online and writing an ebook.

Passive income can be a great option because you can put your efforts into more important things and still make money. But most people aren't interested in working for themselves. So they choose to invest time and energy into earning passive income.

Problem is, passive income won't last forever. You might run out of money if you don't generate passive income in the right time.

Also, you could burn out if passive income is not generated in a timely manner. It is best to get started right away. If you wait until later to start building passive income, you'll probably miss out on opportunities to maximize your earnings potential.

There are three types of passive income streams:

-

There are many options for businesses: You can own a franchise, start a blog, become a freelancer or rent out real estate.

-

Investments - these include stocks and bonds, mutual funds, and ETFs

-

Real estate - This includes buying and flipping homes, renting properties, and investing in commercial real property.

What is the best passive income source?

There are many ways to make money online. Most of them take more time and effort than what you might expect. How can you make extra cash easily?

Finding something you love is the key to success, be it writing, selling, marketing or designing. It is possible to make money from your passion.

For example, let's say you enjoy creating blog posts. You can start a blog that shares useful information about topics in your niche. You can then sign up your readers for email or social media by inviting them to click on the links contained in your articles.

This is called affiliate marketing, and there are plenty of resources to help you get started. For example, here's a list of 101 Affiliate Marketing Tools, Tips & Resources.

You might also think about starting a blog to earn passive income. You'll need to choose a topic that you are passionate about teaching. However, once you've established your site, you can monetize it by offering courses, ebooks, videos, and more.

There are many ways to make money online, but the best ones are usually the simplest. You can make money online by building websites and blogs that offer useful information.

Once you have created your website, share it on social media such as Facebook and Twitter. This is known content marketing.

Statistics

- These websites say they will pay you up to 92% of the card's value. (nerdwallet.com)

- As mortgage rates dip below 7%, ‘millennials should jump at a 6% mortgage like bears grabbing for honey' New homeowners and renters bear the brunt of October inflation — they're cutting back on eating out, entertainment and vacations to beat rising costs (marketwatch.com)

- While 39% of Americans say they feel anxious when making financial decisions, according to the survey, 30% feel confident and 17% excited, suggesting it is possible to feel good when navigating your finances. (nerdwallet.com)

- Shares of Six Flags Entertainment Corp. dove 4.7% in premarket trading Thursday, after the theme park operator reported third-quarter profit and r... (marketwatch.com)

- Etsy boasted about 96 million active buyers and grossed over $13.5 billion in merchandise sales in 2021, according to data from Statista. (nerdwallet.com)

External Links

How To

How to Make Money While You Are Asleep

To be successful online, you need to learn how to get to sleep when you are awake. This means more than waiting for someone to click on the link or buy your product. You can't make money sleeping.

You must be able to build an automated system that can make money without you even having to move a finger. You must learn the art of automation to do this.

It would be a great help to become an expert in building software systems that automate tasks. So you can concentrate on making money while sleeping. You can even automate yourself out of a job.

This is the best way to identify these opportunities. Start by listing all of your daily problems. Then ask yourself if there is any way that you could automate them.

Once you've done this, it's likely that you'll realize there are many passive income streams. Now, you have to figure out which would be most profitable.

For example, if you are a webmaster, perhaps you could develop a website builder that automates the creation of websites. If you are a designer, you might be able create templates that automate the creation of logos.

A software program could be created if you are an entrepreneur to allow you to manage multiple customers simultaneously. There are many possibilities.

Automating a problem can be done as long as you have a creative solution. Automation is the key for financial freedom.